State of the Industry 2026

One hundred and fifteen water professionals participated in the 2026 WaterWorld State of the Industry Survey, providing insight into workforce demographics, financial expectations, infrastructure planning, and the key issues shaping the water sector.

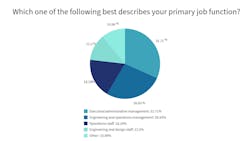

Who is represented in the survey

Roughly one-third of respondents identified their primary role as executive or administrative management, while slightly more than a quarter work in engineering or operations management. Most of the remaining participants serve in operations, engineering, or design roles, with about 10% representing science, research, purchasing, marketing, or sales positions.

Listen to the report with Talking Under Water co-hosts VP of Content Strategy for Water & Energy, Bob Crossen and WaterWorld Head of Content, Mandy Crispin.

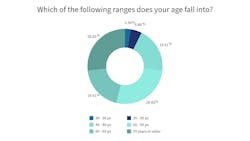

The survey results reflect an experienced workforce. The largest age groups were tied between professionals aged 50–59 and those 70 or older. Overall, respondents aged 40 and above accounted for 93% of participants.

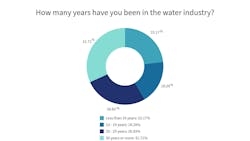

Experience levels have remained relatively consistent in recent years. In 2025, 41% reported fewer than 20 years in the industry, 27% had 20–29 years, and 32% had 30 years or more. Over the past three years, the most noticeable shift has been a gradual increase in the mid-career range.

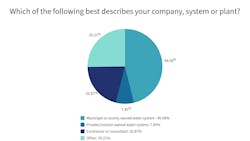

Municipal and county-owned systems again made up the largest share of respondents at 46%, consistent with the previous survey. Representation from private or investor-owned systems declined to 8%, while contractors and consultants accounted for 20%.

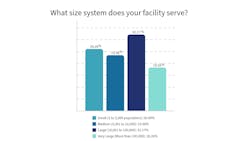

Responses also reflected a balanced mix of system sizes. While the largest share came from large systems and the smallest share from very large systems, the combined totals show nearly equal representation between smaller systems and larger ones.

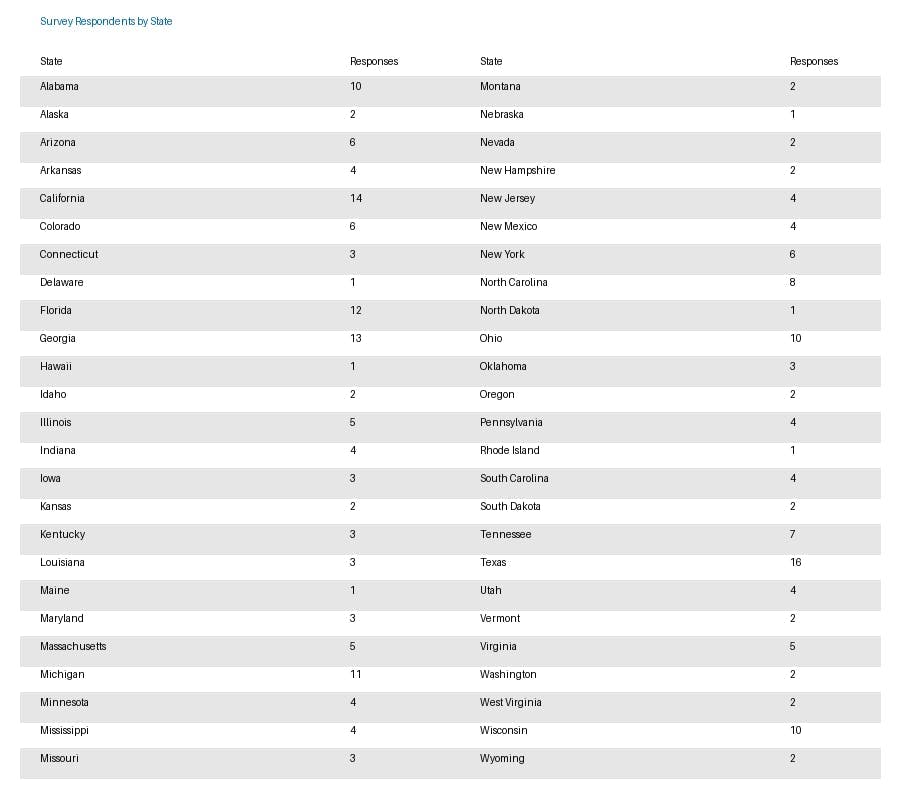

Geographically, Texas produced the most responses for the second consecutive year, followed by California, Georgia, and Florida.

Most respondents reported involvement in purchasing decisions. Only 12% said they were not involved in determining needs, evaluating brands, specifying vendors, or approving purchases.

Costs continue rising while budget expectations remain positive

Operating costs increased for the majority of organizations in 2025. Sixty-seven percent of respondents reported higher costs compared to the previous year, while 22% reported no change and 12% reported decreases.

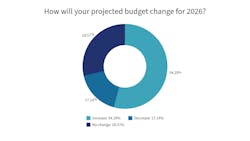

At the same time, more than half of respondents expect budgets to increase in 2026. Fifty-four percent anticipate increases, 29% expect budgets to remain about the same, and 17% expect reductions.

Taken together, these results show that while rising operating costs remain common, most organizations continue to expect stable or growing budgets.

Read more about association plans for 2026.

Revenue expectations trend more cautious

Revenue expectations have shifted over the past several survey cycles. In 2023, half of respondents expected revenue increases. In the 2024 survey results, 42% reported increases, 41% reported no change, and 16% reported decreases.

For 2025, 48% had expected revenue growth. However, this year’s results show that 33% reported revenue increases, 43% reported no change, and 24% reported decreases.

Looking ahead to 2026, expectations for revenue growth have declined compared with earlier surveys. Thirty-eight percent expect revenue to increase, while 46% expect it to remain about the same and 16% anticipate decreases.

Listen to association plans in this episode of Talking Under Water. Forecasting water in 2026: data centers and wastewater association goals with the co-hosts.

Organizational health remains steady

As in previous surveys, respondents largely rated their organizations positively. Most categorized their organizations as being in good or very good health, with smaller shares reporting exceptional performance or significant challenges.

![Chart 10: How would you rate the overall health of your organization today?]](https://img.waterworld.com/files/base/ebm/ww/image/2026/02/698e2137e219198428e5dea2-untitled11.png?auto=format,compress&fit=max&q=45?w=250&width=250)

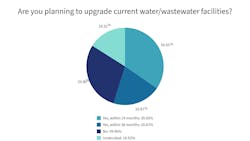

Infrastructure investment remains a priority

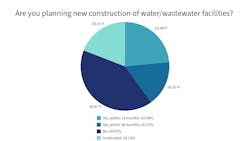

About half of respondents anticipate new construction of water or wastewater facilities within the next three years, while 19% remain undecided. Among those planning construction, responses indicate that many expect projects to occur within the next two years.

Facility upgrades appear even more likely, with 57% planning upgrades within three years, compared with 26% who do not.

Read more about association plans for 2026.

Material pricing and bid costs are also expected to remain key considerations for future projects.

Persistent challenges shape industry concerns

In the 2023 survey, when asked about the most important issues that will affect their organizations in 2024, all the usual suspects showed up: PFAS, regulations, price increases, supply chain issues, tech upgrades/security, aging infrastructure and workforce stressors such as hiring qualified people and retaining them. General inflation concerns were prevalent also.

The foreshadowed concerns of the 2023 survey have come into the light. That year, one person wrote, “Inflation pressure [is] on everything; negative public opinion regarding inevitable rate increases.”

Another in 2023 submitted, “Source Water hands down, we’re going through a drought and the city that supplies us and 8 other municipalities has been affected.

I foresee water conservation as being a huge topic for next year as we need to educate our residents on how to conserve water, shift to growing native shrubs and bushes and get away from grass growth.”

In 2024, there were a lot more open comments about the state of the financial environment and the natural environment.

This year, 2025, regulations, funding, and PFAS, show up as expected. Something unexpectedly prevalent, was the simple response “tariffs.”

Aside from that, and more focused, several comments illustrate the ongoing financial and environmental pressures utilities face. One respondent wrote:

[What] we’ve been facing for several years now and is ongoing are high nitrates. The state comes in and take samples, but there is no help in actually fixing the problem. Their suggestion [is] having a third well. But there is no way the city would ever be able to afford it at this time or in the near future Without any help.

Another respondent described the complexity of funding and water supply challenges:

“Funding! Between Lead Service Line Replacement and State Revolving Funds, we are tapped out for funding. Most remaining projects are R4 total reconstructs, and we fall short on capital to make anything happen.

[Our state agency] using outdated very conservative models doesn't help when asking to add new construction to help off-set cost for existing rate payers either.

Aquifer status is low with less rain fall and available fresh water making our Municipality fight for water with private pocket plants here in [our] County.

Without new rate payers, we have to spend capital to seek other means of water supply, including a regional authority connection.

The issue is that we are a well water system, they are a surface water system and never the 2 shall cross making reinvestment difficult at best and very expensive to say the least.”

A stable but challenging operating environment

Overall, the 2025 survey results point to a sector that remains stable, with many organizations reporting positive health and continued investment plans. At the same time, rising operating costs, cautious revenue expectations, and ongoing regulatory and funding pressures continue to shape the industry’s outlook.

About the Author

Mandy Crispin

Mandy Crispin is the editor-in-chief of WaterWorld magazine and co-host of water industry podcast Talking Under Water. She can be reached at [email protected].